Daily Energy Report

Oil prices and USD, the Haynesville shale play, offshore activities, LNG demand, battery metals, Japan’s first imported “low-carbon ammonia”, China’s Russian oil imports, and more

CHART OF THE DAY: The US Dollar and Oil Prices

Commentary:

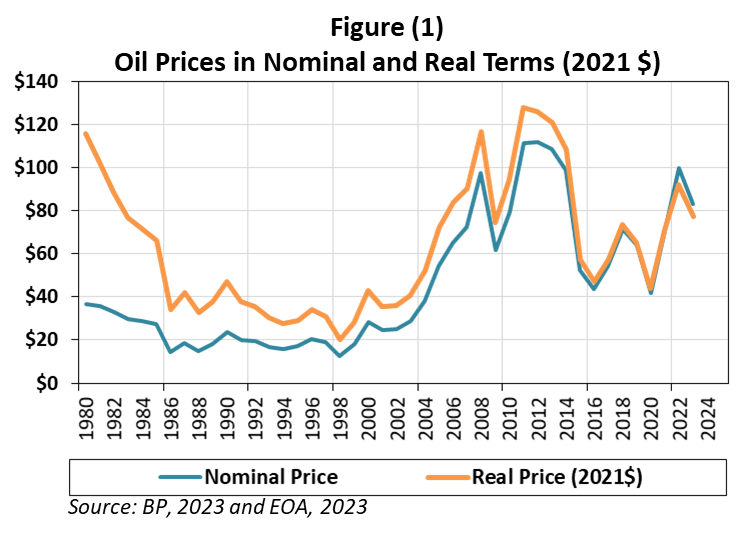

Figure (1) above shows oil prices in nominal and real terms since 1980. Although OPEC was established in 1960, the group did not start implementing the quota system until 1981-1982, and for this reason, our chart starts at 1980.

The chart shows that while today’s oil prices in nominal terms are more than double the average in 1980, they are lower in real terms. In fact, today’s price in real terms is only 66% of what it was in the 1980s. To put it differently, the purchasing power of a barrel of oil in 1980 was higher than today’s by about 50%! However, these figures should not be taken at face value because we also need to account for the terms of trade and exchange rates to count the purchasing power of oil for each oil-producing country.

EOA’s Main Takeaway:

This chart is relevant to a discussion that is gaining ground these days about the future of the US dollar, and whether oil-producing countries should receive revenues in currencies other than the USD.

OPEC tried to ditch the US dollar in the 1970s after the Nixon Administration floated the US currency in 1971. Back then, OPEC members saw the purchasing power of their oil exports— priced in US dollar— plummet. This explains the 70% increase in posted prices just before the 1973 oil embargo. That was compensation for the losses as the US dollar declined in value.

The chart clearly shows how oil loses value in the US dollar. But what’s the alternative? The fact is that using any other currency will have the same problems as the USD, and many of them are way worse. Using a basket of currencies will not work because OPEC members have different trading partners.

Looking at the last two years, oil producers greatly benefited from the rise in the US dollar. The losses would have been worse if pricing and revenues were in a non-USD currency. The question is: what will happen if the dollar depreciates relative to major currencies?

OPEC’s efforts to cut oil production to keep prices relatively high are not meant to only support their budgets, but also to compensate for the losses from the dollar-related inflation and changes in exchange rates. They are trying to maintain the purchasing power per barrel.

In short, OPEC is happy with a higher dollar as long as the increase in the dollar relative to other countries’ currencies is higher than the inflation in exports from these countries to OPEC members. Please keep in mind that the currencies of many OPEC members are pegged to the US dollar in one way or the other.

STORY OF THE DAY

EIA/ENVERUS: Haynesville natural gas production reached a record high in February 2023

REUTERS: Oilfield services giant SLB beats first-quarter profit estimates

Summary:

Dry natural gas production from the Haynesville shale play, the third-largest shale gas-producing play in the US, climbed to new highs in February, averaging 14.4 billion cubic feet per day (Bcf/d), 9% more than the annual average last year which stood at 13.2 Bcf/d, according to the US Energy Information Administration and as reported by analytics firm Enverus.

Production from Haynesville in February made up around 14% of all US dry natural gas production, the report said.

Meanwhile, another oilfield services giant has beaten first-quarter profit estimates this week. Reuters reported today that SLB "beat Wall Street estimates for first-quarter profit on Friday, as elevated crude prices and tight supplies increased demand for its oilfield services." Earlier this week, similar results were reported for Baker Hughes.

EOA’s Main Takeaway:

The general conviction for more than a decade now has been that Haynesville has a lot of gas but is expensive to produce and that the basin is the backyard storage of Japan, South Korea, and China. With the number of LNG plants mushrooming in the Gulf of Mexico region, the argument that Haynesville is for exports have become a reality, and Europe is added to the mix. The additional cost of production makes it competitive once the transportation cost is included. The continuous increase in LNG capacity in the Gulf means that production from the Haynesville shale play will continue to rise.

Regarding the Reuters report on SLB, this reflects the recovery and the record growth in E&P spending in 2022 and the continuation of spending in Q12023. The increased demand for LNG means additional activities as we have seen with the Haynesville shale play.

On a related topic, and as we mentioned before, offshore activities are picking up and we remain bullish on offshore drillers.

NEWS OF THE DAY

1- REUTERS: Japan receives first low-carbon ammonia cargo from Saudi Arabia

Summary:

Japan's first low-carbon ammonia cargo for power generation, and which was sourced from Saudi Arabia, arrived today in the Asian country, Reuters and other media outlets reported. Tokyo plans to use the shipment for co-firing with fossil fuels to cut carbon emissions.

Late last year, Japan inked cooperation agreements with Saudi Arabia in the fields of hydrogen, fuel ammonia as well as carbon recycling, according to media reports.

“The ammonia was produced by SABIC Agri-Nutrients (“SABIC AN”) with feedstock from Aramco and sold by Aramco Trading Company to the Fuji Oil Company (“FOC”). Mitsui O.S.K. Lines (“MOL”) was tasked with shipping the liquid to Japan, then the low-carbon ammonia was transported to the Sodegaura Refinery for use in co-fired power generation, with technical support provided by Japan Oil Engineering Co (“JOE”),” the involved companies said in a joint press statement. The amount of the shipped low-carbon ammonia cargo is unclear.

EOA’s Main Takeaway: