Daily Energy Report

Sub-Saharan Africa’s LNG potential, oil demand in China, seizure of tankers in the gulf, Mexico’s gas plans, drilling in the Arctic, Iraq’s northern crude exports, and more

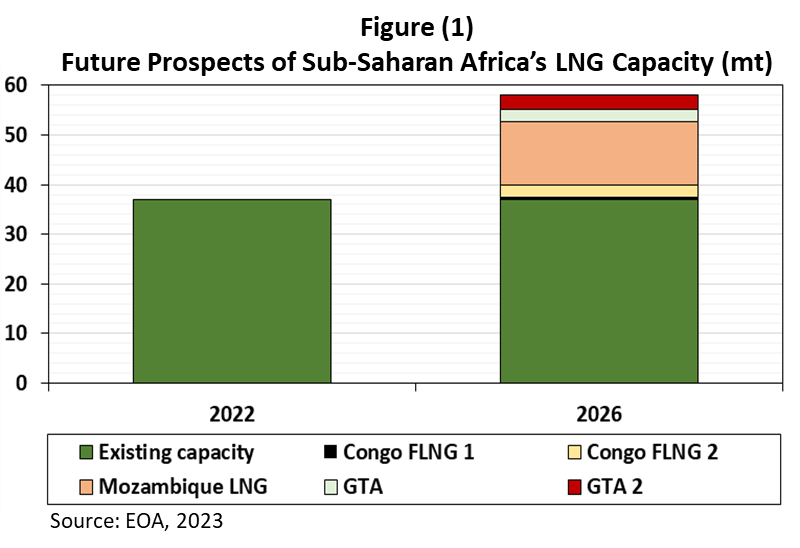

CHART OF THE DAY: Additional LNG Capacity in Sub-Saharan Africa

Commentary

Several new LNG projects are set to come online in the next few years in Sub-Saharan Africa and we discuss a few of them below.

The first phase of the BP-operated Greater Tortue Ahmeyim (GTA) project offshore Mauritania- Senegal is under development and is expected to start operation in late 2023 with a capacity of 2.5 million tonnes per annum (mtpa). On February 23, BP and its partners confirmed the development concept for the second phase with a total capacity of between 2.5-3.0 mtpa. This will bring the total GTA capacity to 5-5.5 mtpa by 2025.

Turning to the Republic of the Congo, the country witnessed on April 25 the launch of its first natural gas liquefaction project during a ceremony attended by Congolese top leaders and officials from Eni— which has been active in Congo for more than 50 years.

The Congo LNG project is expected to reach an overall capacity of 3 million tons per year (approximately 4.5 billion cubic meters/year) starting in 2025, according to a press statement released by Eni.

The project includes the installation of two floating Liquefied Natural Gas units (FLNGs) at the Nenè and Litchendjili fields which are currently in production, and at fields yet to be developed, according to Eni. The first FLNG plant (Tango FLNG), with a capacity of 0.6 mtpa, is now under conversion, and is expected to start production in the second half of 2023, the Italian company said, while the second plant of a capacity of 2.4 mtpa is due to come on stream in 2025. This second FLNG was launched just last December after Eni signed a contract with Wison Heavy Industry for the plant’s construction and installation.

In Nigeria, the government started the construction of a new LNG train (LNG Train-7) in 2022 on the Bonny Island LNG complex with the commissioning date expected by 2024. Once completed, the new train would bring the total capacity of the Bonny LNG complex to 30 mtpa by 2024.

Meanwhile, in eastern Africa, the French energy major, TotalEnergies, is developing the largest LNG project in Mozambique and which has faced delays. Last week, Mozambique’s President Filipe Nyusi said that TotalEnergies can safely resume its operations at the Cabo Delgado LNG project that was halted in 2021 due to attacks launched by ISIS in the northern province, Reuters reported.

Mozambique LNG is the first onshore development of an LNG plant in the country. It includes the development of the Golfinho, and Atum fields located in Offshore Area 1, and the construction of two liquefaction trains (total capacity of 13,1 million tons per annum mtpa), according to a press statement. The delay in the Mozambique LNG project will likely push back the full startup of the project to 2026. For more on this, we encourage readers to check our latest Weekly Newsletter here.

EOA’s Main Takeaway:

The exploration activities made by key energy players have successfully led to a number of massive gas finds in the Sub-Saharan region. By 2026, the region’s LNG capacity could reach 58.2 mtpa, making it a key player in the global LNG market. Despite being relatively small, these projects in the Sub-Saharan African region are important for Europe and Asia for diversification that would enhance energy security.

And since it is all about LNG in the next few years, Sub-Saharan African nations, such as those we discussed in this section, want to have their own share. But it will not be an easy mission. Issues related to security and contracts remain key obstacles to tapping some of these countries’ LNG potential.

STORY OF THE DAY

REUTERS: Chinese tourists return with lighter wallets

Summary:

Reuters wrote today that although Chinese travelers are visiting key domestic areas for tourism, like Shanghai and Hong Kong, they are not spending as expected. Although domestic tourism is supposed to generate more revenues for the country, “spending is lower as many find cheaper ways to have fun."

According to Reuters, domestic tourism revenue is expected "to be just 83% of 2019 levels, at 120 billion yuan ($17.4 billion), according to official estimates, suggesting consumers are opting for lower-cost trips."

EOA’s Main Takeaway:

This is not that bullish! It fits perfectly with our view and which we detailed in the EOA 2023 Oil Market Outlook on January 9. We told readers that most of the growth in oil demand in the first half of the year will be registered in the transportation sector. Demand from other sectors, meanwhile, will be delayed until the second half of the year, and will mostly be seen in the fourth quarter.

What remains to be seen is whether there will be increased spending on durable goods and cars.

NEWS OF THE DAY (9 items)

1- REUTERS: Second oil tanker in a week seized by Iran in Gulf - U.S. Navy

Summary:

The US Navy said today Iran had seized Panama-flagged oil tanker Niovi while transiting the Strait of Hormuz, according to a statement posted on Twitter. This is the second tanker Iran has seized in the Gulf region since Thursday, April 27. The first was the Marshall Islands-flagged Advantage Sweet which was seized in the Gulf of Oman.

EOA’s Main Takeaway: