Daily Energy Report

Daily Energy Report

US power generation by source, OPEC producing above target, EIA’s oil forecasting problem, German LNG deal with Oman, China solar overcapacity, EU’s China turbine imports, and more.

Dear Readers,

We will not publish the Daily Energy Report on Wednesday and Thursday so our Muslim staff members can celebrate Eid al-Fitr with their family and friends. However, in case of major development in the market, we will be in touch.

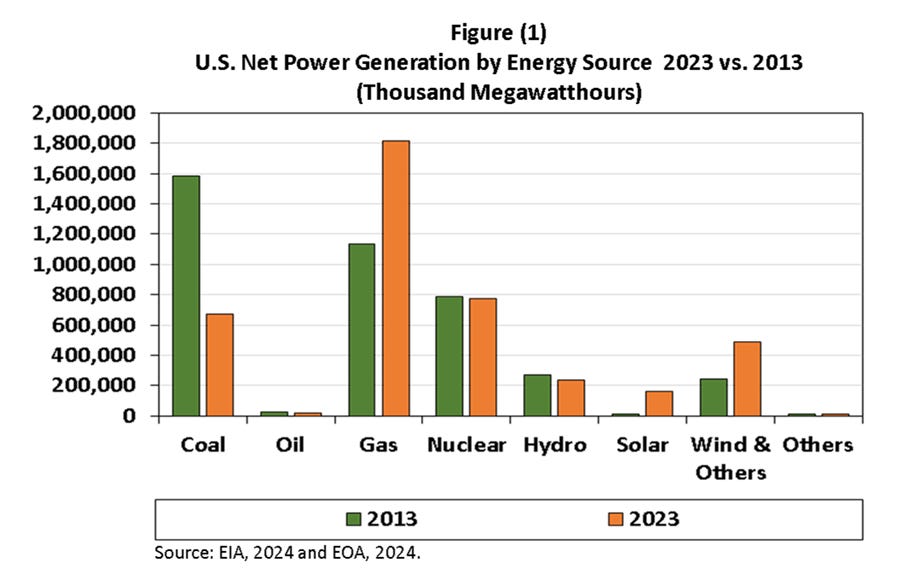

Chart of the Day: US power generation by source

Summary

Figure (1) above shows a comparison of US net power generation in the years 2023 and 2013. The share of coal declined substantially, while the role of gas and renewables increased markedly. Hydro suffered because of the drought in recent years.

EOA’s Main Takeaway

Those who are celebrating the decline of coal as an environmental win and how government policies can be used to fight climate change must awaken to two realities:

While no one can deny that strict government policies forced utilities to close certain coal-fired power plants, it was the abundance of cheap gas that played the bigger role.

As the US reduced its use of coal in power plants, it exported coal to the rest of the world. Those who cheer the closure of US coal-fired power plants cannot reasonably invoke the fight against climate change while that coal is being burned somewhere else. Figure (2) below shows the increase in coal exports and how demand within the US declined.

Story of the Day

Argus: OPEC+ Crude Output Above Target Again

Summary

OPEC+ output surpassed its March target due to overproduction by members like Iraq and Kazakhstan, despite ongoing cuts to support the oil market. Iraq, Kazakhstan, Kuwait, and Gabon were key overproducers. While OPEC was over target, non-OPEC members were under, with Russia close to its goal despite refining capacity damages. Civil conflict in Sudan contributed to underproduction there and in South Sudan.

EOA’s Main Takeaway

We covered the increase in OPEC crude exports a few days ago. This increase in exports, and now this increase in production, answers those who claim that OPEC has been squeezing the market and those who expect prices to exceed $100/b. The market is not that tight.

We noticed that two bullish funds turned bearish in the last couple of days. Today we saw refining stocks get hammered.

Our readers know from previous reports that Iraq, despite cuts, will produce above quota. They also know that neither the Iraqi government nor the Turkish government have an interest in resuming oil exports via pipeline from Kurdistan to the Turkish port of Ceyhan. Since Iraq is cutting production and still producing way above quota, restraining Kurdistan’s production is one way to avoid additional increases and violations.

However, if the market gets tighter in the second half of the year and there is evidence of strong demand and declining inventories, we believe that Saudi Arabia and its allies who cut production voluntarily will increase production. As we have seen in the past, cheaters wait until restrictions are relaxed, then they start counting the increase in their quota and actual production as compensation for past violations. We expect this to happen again.

Table (1) below shows production of OPEC+ who committed to the cuts in March as estimated by Argus. It shows that OPEC members over produced by about 400 kbd while non-OPEC members, on average, under produced by 130 kbd.

Figure (3) shows OPEC crude exports, which we published in a previous report. Exports have been increasing in recent weeks.

News of the Day

EIA: Global Oil Demand is Revised Up, Brent to Average $90 in Q2

Summary

The EIA revised up its estimates of global oil demand for 2022 markedly (yes, 2022, this is not a typo). As a result, its estimates of growth in demand for 2024 and 2025 increased markedly. The EIA increased its growth by almost a half million barrels above previous forecasts.

The EIA revised up its forecasts of oil. It raised its forecast for Brent by $2 in the second quarter to $90/b with an average of $89/b for 2024.

EOA’s Main Takeaway

As our readers know, we stated in our outlooks in the past that we will ignore the EIA’s global oil demand projections because they are out of line, on the low side. Now we know the reason. This is a major flaw in modeling that most researchers fell into. Models include values from previous years. If previous years are wrong, the impact is magnified over time, and you end up with illogical results. That is exactly what we saw in the last two years, and we are glad that we were the only ones who stated publicly that the estimate should be ignored.

However, the fact that the IEA was wrong on US oil supplies for several years and made an accounting fix to the high adjustment, and now we know it was awfully wrong on the demand side in recent years too, we wonder about the impact of such wrong numbers. Here’s a question: why have there been no resignations, and no firing of employees who did their jobs so poorly?

Just to recap: they were wrong on the supply side by about 700-800 kb/d and by about 500 kb/d on the demand side!

S&P Global: Germany's SEFE LNG Deal with Oman Likely Includes Linkage to Gas Hub Price

Summary

SEFE's LNG deal with Oman LNG, set for 2026-2029, is likely tied to the European gas hub index, a shift from typical Middle East contracts linked to crude oil prices. This reflects Europe's growing preference for gas hub index-linked long-term contracts due to its role as a major LNG importer. The Dutch TTF is the expected reference point for pricing in the contract. While Oman LNG usually offers crude-linked prices, this move indicates a possible optimization strategy in the evolving LNG market.

EOA’s Main Takeaway

As LNG becomes a global commodity, we have seen major changes in the nature and details of LNG contracts in the last several months. In general, we see more flexibility than ever that includes shorter durations, new price formulas, and in some cases relaxation of the no resale clauses.

This deal between Germany and Oman is the first of its kind for Oman and also a first for a player in the Middle East. It could be seen as a “calculated new move” in Oman’s strategy to consider other pricing mechanisms in addition to the traditional scheme based on oil indexation. Any negative impact on Oman from such a contract is limited since the contracted volume with SEFE is small and for a short time. But there could be some strategic advantage of having such a contract with Germany.

Will other players in the region, such as Qatar and the UAE, follow suit? No. Qatar and the UAE are building greenfield projects that require long term contracts with more price stability that are linked to oil. They need such long-term contracts with this type of pricing to cover CAPEX and OPEX along the contract duration.

We believe that Qatar and the UAE could consider this pricing mechanism or something similar in the “renewal” of some legacy contracts from the operating facilities that expire in the next few years.

Bloomberg: European Gas Swings Near 2-Week High with LNG Diverted to Asia

Summary

European natural gas prices have climbed, with gas being shipped to Asia and reduced Norwegian supply due to maintenance contributing to the rise. While Europe’s mild winter has left high gas inventories, it still faces competition for LNG due to reduced Russian pipeline gas. Currently, the flow of LNG to Asia, Brazil, and Egypt is not strong. LNG deliveries in northwest Europe are below the five-year average, but high wind generation in the UK is mitigating price increases for now.

EOA’s Main Takeaway

The EU exi ted the withdrawal season with the highest gas storage on record, as we have discussed before. A mild winter with high storage reduced gas prices in Europe relative to Asia and led to the diversion of LNG carriers to Asia. Now the filling season has started but shipments are being diverted. The result has been higher prices in Europe.

However, such a development is positive because it is one of the signs of the LNG market becoming international.

WSJ: AI’s “Insatiable” Energy Needs Not Sustainable, Says Arm CEO

Summary

Arm, known for reducing power usage in smartphones, is now emphasizing energy efficiency in AI. AI's heavy power consumption could lead to data centers using up to 25% of US power by the decade's end. The IEA reported that an interaction with ChatGPT uses 10x more electricity than a Google search, with AI power demand projected to grow 10x by 2026. Arm CEO Rene Haas said the trajectory of AI’s energy consumption is not sustainable.

EOA’s Main Takeaway

This is a never-ending story: remember the rebound effect from energy efficiency? Our homes are more energy efficient, but now they are larger than ever (Jevon’s Paradox)! Such technology is needed, but it doesn’t change the upward trend in energy consumption. It just reduces the rate of growth. This is an important conclusion, especially for policymakers: unrealistic policies will fail and their costs will be very high. Reasonable, practical policies are needed. Let us remember that data storage and data centers were not in the picture 30 years ago. Bitcoin and crypto currencies were not in the energy picture 10 years ago. Now we are realizing how AI will consume even more than everything we have experienced before.

Bloomberg: Market Forces, Not Words, Can Fix China’s Solar Overcapacity

Summary

China's clean-energy production boom is causing concerns about global overcapacity. However, China's solar manufacturers face their own challenges due to an oversupply leading to plummeting prices and operational cutbacks. The situation is complex, fueled by aggressive expansion and rapid technological advancements. While international pressures won't easily resolve overcapacity, Chinese firms are responding by expanding manufacturing abroad.

EOA’s Main Takeaway

Secretary Yellen and members of the Biden Administration must realize the overproduction was fueled by government subsidies both inside and outside of China. Blaming Chinese manufacturers for overproduction is nonsense. They responded to government incentives around the world. You cannot talk about “market forces” until you eliminate government subsidies around the world, especially in Europe and the US.

As for expanding abroad, this has nothing to do with the surplus. It has everything to do with trade wars, restrictions, and tariffs. The only way Chinese manufacturers can circumvent the tariff is by building factories in countries like Mexico where tariffs would not apply. They may also move to the US and—guess what—get subsidies from the US government! See the news item below!

Reuters: EU to Investigate Chinese Turbine Suppliers to Wind Parks

Summary

The European Commission is investigating subsidies to Chinese wind turbine suppliers involved in European wind projects, amid concerns over China's increasing influence in the clean tech sector. This follows investigations into Chinese EV imports and is part of a strategic shift to prevent market dominance like that seen in the solar panel sector. The inquiry is enabled by the EU foreign subsidies regulation, which checks if foreign subsidies lead to unfair public tender bids.

EOA’s Main Takeaway

When will the EU governments realize that their green revolution is China’s economic survival strategy? When will they understand that they cannot have their cake and eat it too? The fact is, the EU cannot do much. They are so dependent on China they cannot cut the umbilical cord!

WSJ: Chevron Exits Myanmar with Withdrawal from Natural Gas Project

Summary

Chevron has officially exited Myanmar, divesting from the Yadana natural gas project after announcing plans to leave following the country’s military coup. Chevron’s 41% stake has been redistributed to the project's remaining shareholders, Thailand’s PTTEP and Myanmar’s MOGE. This move is part of a broader trend of international firms withdrawing from Myanmar due to political turmoil and sanctions since the 2021 coup.

EOA’s Main Takeaway

How many years did it take for Chevron to exit Myanmar? This is an important lesson for those who are waiting for a major decline in Russian oil production!

Chevron was under massive pressure, not only because of sanctions, but from various human rights groups, religious congregations, and investors, to leave the country.

Bloomberg: Lithium Market Struggles to Recover after Epic Boom and Bust

Summary

Lithium prices are stabilizing. The market has seen volatility due to a mismatch between the supply surge and EV demand. While some expect prices to rise, a more diverse mining landscape could prevent extreme boom-and-bust cycles. Challenges include refining capacity and the potential for carmakers to seek alternatives to lithium if prices become too unstable.

EOA’s Main Takeaway

The natural resource business is cyclical by its nature. It requires massive investment upfront and involves huge sunk costs. Once you start producing, what matters is to keep your head up in deep water, and the focus shifts to operational costs instead of total costs: produce so long as the price is above the operating cost.

The situation became worse as the growth in demand for electric vehicles turned out to be way lower than expectations.

Reuters: Swiss Climate Policy Shortcomings Violated Human Rights, Court Rules

Summary

The European Court of Human Rights ruled that Switzerland breached citizens' rights by not adequately addressing climate change, following a case by Swiss women citing risks from heatwaves. This landmark decision sets a precedent for climate-related legal actions based on human rights. The ruling may force the Swiss government to strengthen its emission reduction efforts to align with the Paris Agreement's targets.

EOA’s Main Takeaway

While fossil fuels may be having some impact on the climate, there is no credible way for scientists to separate the impact of human activities from natural variations in climate cycles, which can last for years, decades, and even centuries. Considering this fact, how can any court rule that citizens’ rights are being violated? Legal activism could become an even greater danger to the world’s energy systems. However, we remain optimistic that once electricity and fuel reliability becomes a problem that directly impacts people’s lives in a serious way, the public will insist that this kind of legal activism be minimized.

The fear, and this goes both ways, is that the judiciary will become more powerful than ever, and the job of politicians will be to choose the judges. In this case we end up with a dictatorship disguised as the “law”.

Bloomberg: European Nuclear Plants Put Out of Work by Green Power Surge

Summary

The rise of renewables in Europe is challenging the nuclear industry, with high renewable output and low power prices causing nuclear plants to lose market share. Energy demand hasn't fully bounced back, leading nuclear operators like Electricite de France to occasionally idle plants. Current trends suggest nuclear may get edged out by renewables, which continue to grow rapidly across the EU.

EOA’s Main Takeaway

This article is propaganda. Electricity prices across Europe are not cheap. Yes, there are some countries that have experienced surplus power supplies, but this is not the norm. Introduce just one heatwave or extended cold snap with dramatic reductions in wind/solar output and many European nations will experience blackouts. Europe, like the rest of the world, needs more nuclear power.

Our problem with Bloomberg news stories is always the same: journalists inject their views into news items. One plant, one country, and the writer, without any evidence, extrapolates that to the whole industry and to the rest of the world. We will refer to this story in the future.

Other News

EIA: US Refiners and Chemical Manufacturers Lead Hydrogen Production & Consumption

Bloomberg: BP Sees Strong Trading Performance in First Quarter

Reuters: US Must Secure Africa Ties to Secure Key Minerals

Bloomberg: Trafigura is Incredibly Bullish on Power Demand

Reuters: Vitol’s Foray into Metals Not a Strategic Pivot Away from Energy