Daily Energy Report

EU gas imports by source, US crude inventories, US gas prices to rise, BP outlook, BP ‘transition’ propaganda, EU tariffs & EVs, Hyundai accused of faking sales, VW’s EV slump, and more.

Chart of the Day: Although EU Demand for Gas Declined in June, about 18% of Gas Imports Came from Russia

Summary

Figure (1) above shows the EU’s natural gas imports by source. LNG accounted for 40.2% of the EU’s total gas imports (including LNG), while pipeline gas accounted for the remaining share at 59.8%. In June, Norway supplied 33.3% of the EU’s total gas imports, while US LNG accounted for 17.3% of the bloc’s total imports. Russia (including its LNG) has retained a share of 17.9%, surpassing Algeria (piped gas and LNG) which supplied 15.7% of the EU’s total imports.

EOA’s Main Takeaway

LNG continues to play a significant role in the EU’s gas supply mix since Russia’s invasion of Ukraine. But the competitive LNG market is not devoid of challenges for the EU, especially if demand in Asia continues to increase, or in case of severe hurricanes in the Gulf of Mexico, as we discussed in the past.

The EU’s LNG imports last month sharply dropped by 5.8% month-on-month, reaching 6.8 million tons (equivalent to 9.3 Bcm of degasified LNG), according to data from Kpler. This significant drop was due to muted demand amid full gas stockpiles. France was the top importer in the region with 1.63 Bcm, followed by the Netherlands with 1.59 Bcm, and Spain with 1.58 Bcm.

From the LNG supply side, the US remained the EU’s top LNG supplier, accounting for 42% of delivered LNG cargoes into the bloc, followed by Russia with a share of 20%, Qatar (14%), and Algeria (10%).

Story of the Day

EIA: US Crude Oil Inventories Declined by 3.44 MB

Summary

US crude oil inventories declined by 3.443 mb to 445.1 mb last week, according to the EIA, as shown in Figure (2) below. Gasoline inventories declined by 2.006 mb to 229.7 mb while distillate inventories increased by 4.884 mb to 124.6 mb.

Crude imports increased by 0.214 mb/d to 6.760 mb/d. Crude exports declined by 0.402 mb/d to 3.999 mb/d.

Refinery utilization increased from 93.5% to 95.4% last week, as crude inputs into refineries increased by 339 kb/d.

EOA’s Main Takeaway

Although the decline in crude inventories came in higher than expected, the biggest surprise came from the large increase in distillate inventories. Although prices increased today, the increase was small and Brent prices remain below $85/b. We maintain our view that without any major political events, prices will move sideways. US crude inventories must decrease significantly to have an impact on oil prices.

News of the Day

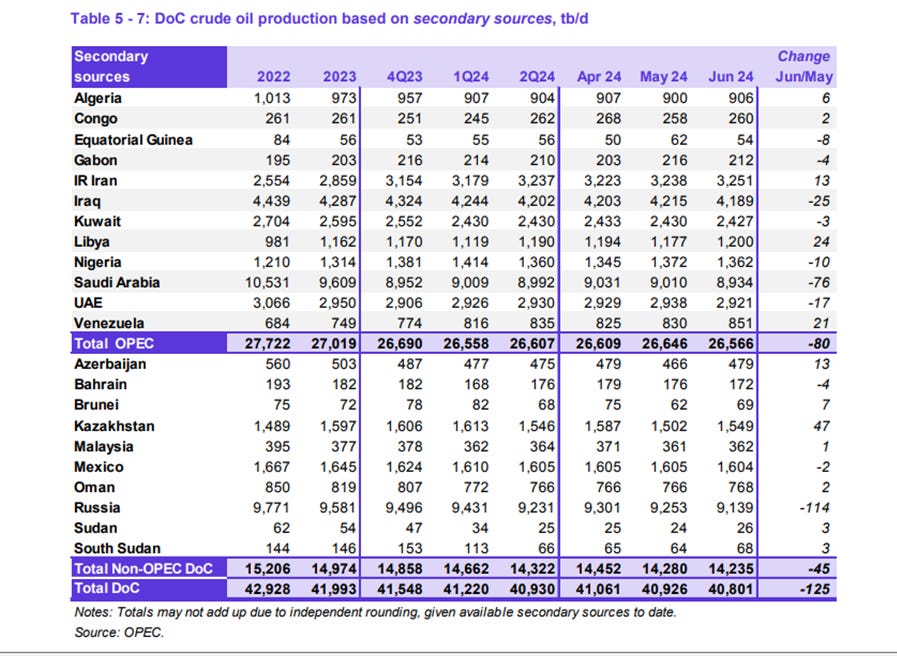

OPEC: OPEC+ Production Declined in June by 125 KB/D

Summary

Based on independent secondary sources, OPEC production declined by 80 kb/d last month. Most of the decline came from Saudi Arabia, followed by Iraq, as shown in the table below. Production of members of OPEC+ who are not members of OPEC declined by 45 kb/d. Most of the decline came from Russia, but some of this decline was countered by an increase in Kazakhstan’s crude production.

EOA’s Main Takeaway

The decline in Iraq’s crude production was much lower than promised.

Iraq produced 185 kb/d above the target in June. Kazakhstan increased production instead of cutting it as promised. It is producing 79 kb/d above quota. Russia also produced above target by 135 kb/d.

As we have mentioned before, it seems the game plan for those countries is to wait until the fourth quarter when OPEC+ will start unwinding production. By then, the ceiling will be higher than production. They will count the difference as compensation for earlier increases in production. It will be a serious problem for OPEC if growth in global oil demand remains weaker than expected and is forced to halt the unwinding. Compensation for earlier increases then becomes a serious problem.

Figure (3) below shows OPEC crude oil production. If current production levels are maintained next month, it will exceed that of last year.

On a related front:

Reuters: OPEC Sticks to 2024 Oil Demand View, Sees Strong Travel Season

Summary

OPEC maintains its forecast for robust global oil demand growth in 2024, expecting a rise of 2.25 mb/d and 1.85 mb/d in 2025, unchanged from last month. OPEC anticipates strong fuel demand during the summer in the Northern Hemisphere. The forecast contrasts with BP's prediction of oil demand peaking next year. OPEC+ has been supporting the market with output cuts since late 2022.

EOA’s Main Takeaway

We still think that the OPEC demand forecast is overly optimistic for several reasons. US numbers show record numbers of passengers traveling by air, but jet fuel has not picked up yet as we have discussed in previous reports.

Bloomberg: US Natural Gas Bulls Finally Get Some Good News

Summary

US natural gas prices are forecasted to surge by over a third in the second half of the year, according to the EIA. This follows an oversupply due to a warm winter, leaving storage levels 18% above the five-year average. Prices have struggled to exceed $3 per MMBTU. The forecasted average price for the second half is $2.90, up from $2.10 in the first half. For this prediction to hold, a cold start to November is needed to reduce storage levels quickly.

EOA’s Main Takeaway

While this fits with most forecasts, including ours, we should be mindful of three facts that are all related to the expected severe hurricane season in the Gulf of Mexico (GoM):

They reduce gas production, which is bullish for prices.

If refineries stop working, natural gas demand declines, which is bearish for prices.

Delays in LNG shipments either because of hurricane passage or damage. (This is the most bearish case for natural gas prices in the US, as gas is backed out in the pipelines.)

The point here is this: what is the net impact? In general, it is bullish unless one of the major LNG plants stops operating!

Reuters: BP Energy Outlook: Both Main Scenarios See 2025 Oil Peak, Rapid Renewables Growth

Summary

BP's Energy Outlook predicts oil demand will peak next year, and wind and solar capacity will grow rapidly under both main scenarios. In the Current Trajectory Scenario, primary energy demand rises until the mid-2030s, then plateaus to 2050. Oil demand peaks at 102 mb/d by 2025, declining to 75 mb/d 2050. Natural gas demand grows by 20%, with LNG demand rising 40% by 2030. Wind and solar capacity increase eight-fold by 2050. In the Net Zero Scenario, energy demand peaks in the mid-2020s, then declines by 25% by 2050. Oil demand falls to 25-30 mb/d by 2050. Natural gas demand peaks mid-decade and halves by 2050. LNG demand rises 30% by 2030 but declines 40% by 2050. Wind and solar capacity increase 14-fold by 2050.

Figure (4) below is a copy from BP Outlook. It shows that the company expects global oil demand to peak in 2025.

EOA’s Main Takeaway

Our answer is this:

https://x.com/anasalhajji/status/1689461823404195841

Bloomberg: BP Warns of “Disorderly” Clean-Energy Transition amid Record Fossil Fuel Use

Summary

BP warned that the world's shift from fossil fuels to clean energy is too slow to avoid severe climate change, increasing the risk of a "disorderly" transition. Fossil fuel consumption broke records last year, and both low-carbon energy and fossil fuels are still on the rise. The report noted a slow transition could lead to significant economic and social costs. Efficiency improvements have been minimal, with global oil demand expected to grow until the end of the decade. To achieve net zero carbon emissions, BP projects that oil use must drop 70% by 2050.

EOA’s Main Takeaway

Nonsense! This is pure propaganda that is beginning to sound like desperation. BP warns of “significant economic and social costs.” This is bad analysis for several reasons, but here are the top three:

Why don’t BP’s analysts examine the negative outcomes of the alternative? Attempting to reduce global oil use by 70% by 2050 will incur enormous costs across every sector. We argue that these costs are significantly higher than the impacts of a moderate amount of temperature increase over the next quarter century. Our characterization of “significantly higher” is probably an understatement.

BP’s prediction makes the giant assumption that is tenuous at best. It assumes that a relatively small amount of CO2 emissions by humans (in comparison to natural emissions) is wreaking havoc on the world’s climate. Where is the evidence of such a dramatic assessment? There is no way to separate human impacts from natural impacts. It’s entirely plausible, perhaps likely, that the impact of human-generated CO2 emissions has little to no meaningful impact on the climate.

BP assumes that if the world manages to dramatically reduce CO2 emissions without destroying the world economy that this will slow the warming and climate disruption some scientists say is due to human activities (recent studies are demonstrating that CO2 emissions impacts and changes to the climate are exaggerated). There is no evidence available that would credibly support this assumption.

Aside from the BP failures mentioned in our takeaway, we would like to remind readers that BP spent $200 million on its "Beyond Petroleum" ad campaign… 25 years ago!

Wood Mackenzie: Could New EU Tariffs on China Imports Slow EV Adoption?

The BYD Explorer (1), loaded with vehicles, sets sail from Yantai, China, om Jan 10, 2024. Source; Fortune, 2024.

Summary

The European Commission plans to impose tariffs of 17.4% to 37.6% on Chinese EV imports to boost EU EV manufacturing. These tariffs aim to give European carmakers time to scale up, incentivize Western OEMs to produce in the EU, and encourage Chinese OEMs to invest locally. Currently, 20% of Europe's EVs are from China. If made permanent, the tariffs will increase EV costs despite subsidies. Support varies: France is strongly for them; Germany and Sweden oppose due to different market impacts.

EOA’s Main Takeaway

All trends point to slower growth in EV sales than earlier forecasts. However, China can still avoid the tariff through transshipments and assembly factories in other countries. China is moving assembly lines to countries like Vietnam, Morocco, and Mexico. In other words, the impact of the tariff is limited.

Bloomberg: €130 Billion Nuclear Dream in Europe Meets Financial Reality

Summary

Eastern Europe plans to build a dozen new nuclear units costing nearly €130 billion, with the first operational within a decade, to replace aging Soviet-era plants. However, funding and expertise are challenges, requiring government support and EU subsidies. Western Europe is divided on nuclear. Belgium and Spain plan phase-outs, Austria rejects it, and Germany is abandoning it. Belgium, France, Finland, and Sweden rely heavily on nuclear energy.

EOA’s Main Takeaway

We all know now the energy transition is inflationary any way you look at it. The difference is, either you try, spend your money, and move from one energy crisis to another, or suffer in the short run to avoid problems in the longer run. Nuclear is the way to go despite near-term pain.

Bloomberg: Dozens of Sanctioned Russian Oil Tankers Are Sitting Idle All Over the World

Summary

Dozens of tankers previously transporting Russian oil are now idle due to US, UK, and European sanctions, primarily targeting ships breaching a G7 price cap on Russian oil. Since October 2023, 53 ships have been sanctioned, with most failing to load cargo since. While freight rates are falling, indicating that sanctions disrupt tankers, they don't significantly increase Russia's costs for individual cargoes.

EOA’s Main Takeaway

This a recycled news. There is an irony here. News outlets were complaining about Russia using old and unfit oil tankers that could cause an environmental disaster. Now many of those tankers are idle. But where is the talk about the environmental benefits of this change! Additionally, it is clear from various indicators that growth in global oil demand is weak, as many OPEC+ producers are cutting production. It is only normal to have some idle tankers. Which tankers does an operator use and which ones does the operator idle? Of course, the operator idles the sanctioned tankers. If OPEC+ decided to go with the implementation of the unwinding of production cuts in the fourth quarter, more tankers will be needed. That will be the ultimate test. Will those tankers go back to loading Russian oil? Keep in mind, some of those tankers have changed ownership, flags, and locations!

Reuters: Lawsuit Accuses Hyundai of Faking US Sales Data for EVs

KONA Electric. Source, Hyundai, 2024.

Summary

A group of Hyundai Motor dealers sued Hyundai Motor America Corp in Chicago federal court, alleging the company inflated EV sales numbers and punished franchises that did not participate. The lawsuit claims Hyundai pressured dealers to misuse inventory codes to exaggerate sales figures, rewarding those who complied with discounts and incentives. The lawsuit claims Hyundai's scheme gave desirable inventory to fewer dealers, misled the public about demand, and deprived customers of choice.

EOA’s Main Takeaway

This is just an amazing story! If proven, it will change the whole outlook for EVs and will explain why gasoline demand is not declining proportionally to EV sales..

This is no different from the VW emissions fiasco: Volkswagen emissions scandal

Investing.com: Volkswagen May Close Brussels Factory as Low EV demand Hits Audi

Summary

Volkswagen warned it might close Audi's Brussels plant due to a sharp drop in demand for high-end EVs. The potential closure would be Volkswagen's first plant shutdown since 1988 and could cost up to €2.6 billion in the 2024 financial year. The Brussels plant, which employs around 3,000 people and built 50,000 cars last year, faces structural challenges and high logistics costs.

EOA’s Main Takeaway

Again, we are seeing more a retreat from climate change policies everywhere. Projected growth for EVs was overestimated by a huge margin. Analysts believed growth in EV adoption would be similar to growth in car adoption after the horse and carriage. They thought it would be like the adoption of phones, smart phones, TVs, and microwaves. Living in this bubble of thinking is what made EV sales disappointing to them.

They missed the fact that the earlier trend of large growth was caused by true “believers” of certain political positions and certain views of the world who are well off and would buy an EV, regardless of cost. Once that group was satisfied, growth for the rest of the population was a function of personal economics, not only financial costs, but all other considerations.

Also, there is some analytical confusion out there about what constitutes an “affordable” EV. Making a cheap, small, no-frills EV with a lower range is not “affordable”. “Affordable” means making good EVs with a long range and all the bells and whistles at a lower cost than comparable ICE cars.

EIA: West Coast Summer Refinery Margins Decline Despite Reduced Capacity

Summary

This spring, California refinery crack spreads for gasoline and diesel fell below average despite reduced West Coast refinery capacity. The decline is due to growing gasoline inventories and increased biofuel use replacing diesel. In early May 2024, Los Angeles gasoline crack spreads dropped below the five-year average. Despite reduced capacity, regional gasoline crack spreads fell as production increased after maintenance and gasoline consumption decreased. Diesel prices remain closer to average due to low distillate inventories, though renewable diesel growth is muting the effect.

EOA’s Main Takeaway

Experts agree on all the points mentioned in the story above, especially the role of biofuel.

However, the story ignored other facts. Gasoline and diesel prices are not just high. They are the highest in the nation. The impact is clear: lower quantity is demanded. Also, economic growth remains weak despite recent improvement. Most of the growth came from improvement in productivity while the labor market remains weak as unemployment increased. An increase in unemployment means lower income and that translates into lower fuel demand.

Other News

Reuters: India Races to Build Power Plants in Region Claimed by China

Bloomberg: Chinese Solar Company Longi Forecasts First-Half Loss as Prices Drop

XM: Waldorf Production Administrator Puts North Sea Assets on Sale

Reuters: Honeywell to Buy Air Products’ LNG Unit for $1.81 Bln

Reuters: Saudi Arabia Raises $12.35 Billion from Aramco Share Sale after Increasing Offer