Daily Energy Report

Germany’s LNG regasification capacity expansion, Europe’s gas and electricity markets, IEA’s global EV outlook, Russia’s tit-for-tat measures, Mozambique’s gas ambitions, EIA inventories, and more

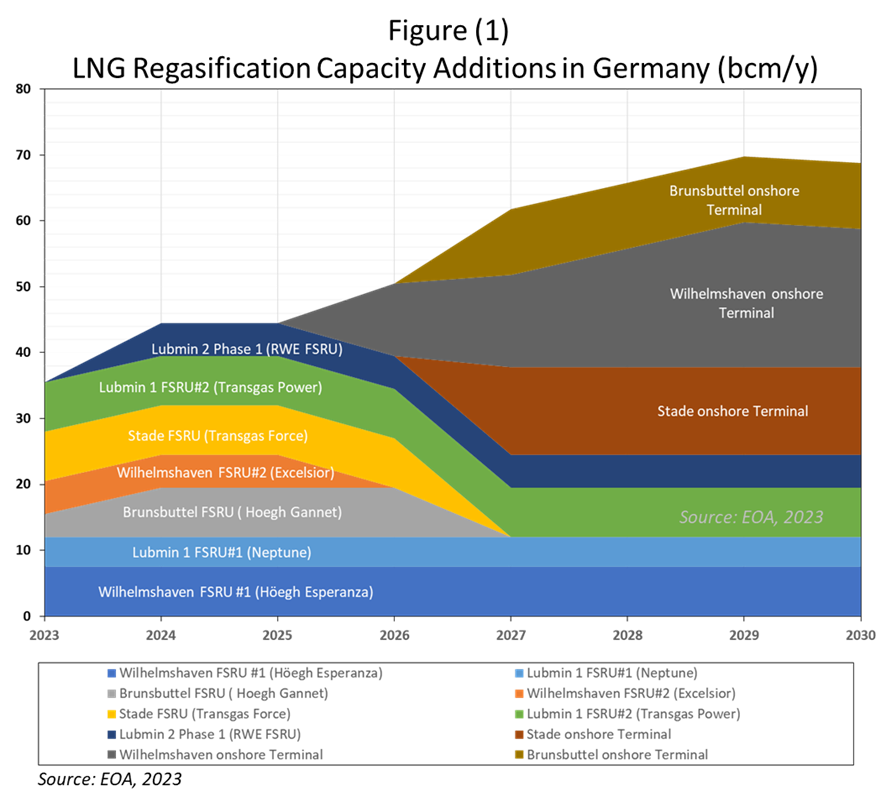

CHART OF THE DAY: Germany’s LNG Regasification Capacity Expansion

Commentary:

Figure (1) above shows how the German government, along with the private sector, plans to replace most of the leased floating storage and regasification units (FSRUs) with land-based units.

Historically, Germany has never imported LNG because it lacked the necessary import facilities. There was always no business case to attract investments in infrastructure and import costly LNG instead of cheap Russian piped gas. Then came the Russian invasion of Ukraine.

Berlin has taken a series of short and long-term actions to shift away from Russian gas and halt any remaining flows by the summer 2024. To reach that end, Germany has secured a dozen of LNG projects to access the global LNG market. The Federal Government initiated a plan to lease five FSRUs units to rapidly add LNG capacity over four locations in Wilhelmshaven, Lubmin, Brunsbuttel, and Stade. In the medium term, the government plans to develop one onshore (land-based) terminal in Brunsbuttel to replace its chartered FSRU, the Hoegh Gannet, to provide a permanent LNG import solution.

Another three government-backed FSRUs are set to enter service by the end of 2023, boosting the combined LNG import capacity to some 36 bcm/year. The list includes a second FSRU in Wilhelmshaven where E.ON, TES, and, Engie will deploy the FSRU, Excelsior, with a capacity of 5 bcm/y. Stade is expected to welcome its 7.5 bcm/y FSRU, the Transgas Force, in winter 2023/2024, while Lubmin is scheduled to receive its second 7.5 bcm/y FSRU, the Transgas Power, in the fourth quarter of this year.

In parallel with the government plans, the private sector is interested in developing four projects over three locations in Lubmin (two FSRUs), as well as one onshore terminal in Stade (developed by Hanseatic Energy Hub (HEH), with a capacity of 13.3 bcm/y) and Wilhelmshaven (developed by Tree Energy Solutions (TES) with a capacity of 18-22 bcm/y). The private sector is more interested in investing in fixed regasification capacity than the government which is more focused on rapid floating solutions. On April 18, Hanseatic Energy Hub awarded the contract for the design and development of the Stade terminal to a consortium led by Spanish firm Técnicas Reunidas. The project is worth 1 billion euros and is expected to come online by 2027. The terminal will also prepare the market for the ramping up of hydrogen.

These projects will enable Germany to have the fourth-largest LNG import capacity by the end of the decade behind China, Japan, and South Korea. Since the beginning of 2023, three FSRUs have started operations in three different locations— in Wilhelmshaven, Lubmin, and Brunsbuettel— adding a combined LNG import capacity of 15.5 bcm/year. This is equivalent to one-third of Germany’s gas needs.

EOA’s Main Takeaway:

It is evident that the FSRU option is being adopted to rapidly start importing LNG to fill the supply gap and boost energy security as a result.

Germany’s LNG option is the most significant development in the country’s energy sector since it ended its reliance on Russian gas and closed its last nuclear reactor. However, the problem now is that Germany is dependent on the spot market for gas supplies and expensive LNG. It has also shifted its dependence on gas imports from Russia to other countries, including the US. But US LNG comes with significant risks as we discussed in this report: Dangers of Europe’s Dependence on US LNG.

STORY OF THE DAY

MCKINSEY&COMPANY: A balancing act: Securing European gas and power markets

Summary:

To address the fall in gas supply last year following Russia’s invasion of Ukraine, Europe had to reduce natural gas consumption by 57 billion cubic meters (bcm). If Europe wants to maintain the supply-demand balance it managed to strike in 2022, it will have to further lower demand and secure new sources of natural gas, according to a recent article by Mckinsey&Company.

“Multiple drivers could create a low-supply scenario and Europe would need to reduce its consumption from 2022 levels by another 55 bcm in 2023 to stabilize the market,” the article says.

According to the piece, the drivers that could affect supply include: 1) a rebound in Asian demand which will likely create competition between Europe and Asia over LNG cargoes, and 2) a complete halt in Russian piped gas which will translate into a supply fall of 25 bcm from Q42022.

Meanwhile, and regarding the demand side, a colder winter this year could increase gas demand by another 15 bcm, while reducing demand in the power sector could help cut gas demand by 14 bcm.

However, the article notes that despite cutting demand in the power sector, gas can contribute to lower overall gas demand in the near term, the sector is heavily reliant on gas-fired power. “As gas power generation determines the marginal price on the power generation merit order curve, nearly tripling the gas price from €70 to €200 per megawatt-hour would likely only decrease gas demand from the European power sector by 8 percent but increase power prices by 70 percent,” the article says.

Meanwhile, if gas demand for heating in buildings does not undergo any changes, Europe may be able to keep saving around 19 bcm.

The article also says that the new LNG regasification capacity of 70 bcm which is due to become available in the next two years, could allow Europe to sustain supply-demand balance and avoid a jump in prices.

In the near term, however, Europe still needs to undergo additional demand reductions to be prepared for any possible price shock later this year and to keep its energy markets in balance. The business community will have to contribute to European efforts seeking to maintain the equilibrium. “Businesses may need to implement near-term measures now, but also start considering the longer-term measures that require upfront capital expenditures,” the article says.