EU Gas Supply Mix: Russian Gas Hits All-Time Low

Main Takeaway

The EU gas imports from Russia reached an all-time LOW in January. However, it is unclear yet if such imports will remain at these low levels when EU member states start refilling their gas stockpiles to prepare for the next heating season.

In Detail

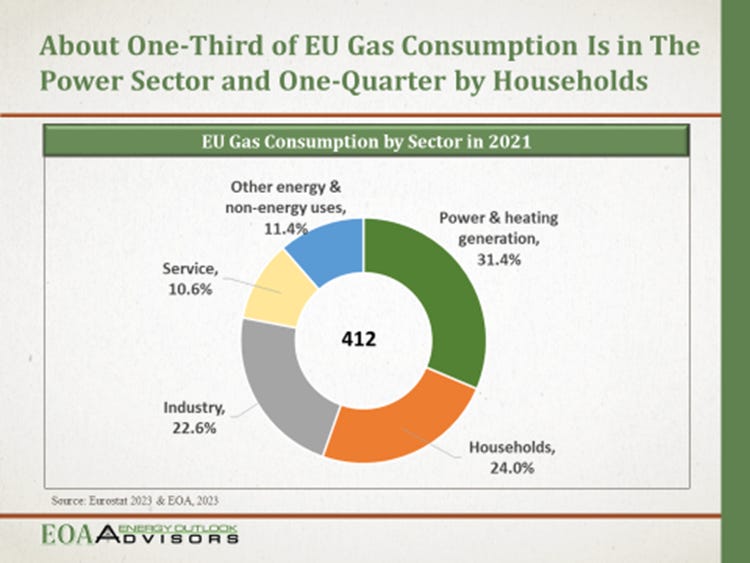

One of the most noticeable implications of the Russia-Ukraine war on the energy industry is the declining role of Russian gas in the EU’s gas supply mix. Prior to the war, Russia was the EU’s top gas supplier. In 2021, EU countries consumed about 412 billion cubic meters (bcm) of natural gas, of which Russia supplied 155 bcm, accounting for around 38% of total gas consumption in the bloc. Gas in the EU is mainly used in the electric power sector, as well as in the residential and industrial sectors. Data from Eurostat shows that about one-third or 31.4% of gas is consumed in the power sector, one quarter (24%) is used by households, 22.6% is used in the industry sector, while the remaining share is distributed among the service sector and other energy and non-energy uses as shown in Figure (1) below.

Figure (1)

Russian Piped Gas Supplies Hit New Monthly All-Time Low

Following Russia’s invasion of Ukraine, the EU has taken concrete actions to diversify its gas sources by importing additional volumes from other suppliers, and sharply increasing its imports of LNG, particularly from the US. Norway, Algeria, and Azerbaijan are currently the EU’s main gas suppliers and have emerged as reliable alternatives to assist the bloc in its efforts to wean itself off Russian gas.

To assess the success of European efforts to shift away from Russian gas, the EOA has issued a monthly tracker of piped gas supplies to the EU from Russia, Azerbaijan, Norway, and North Africa (Algeria and Libya), as well as LNG cargoes from the global market. This tracker aims to highlight changes in gas supplies to the EU, and how new sources were able to help reduce the bloc’s reliance on Moscow.

According to the EOA’s calculation for January 2023, Russia transported 1.8 bcm of gas to Europe (including Ukraine) via Ukrainian territories and through the TurkStream pipeline (passing through Turkey), down from 2.5 bcm a month ago and sharply down from 7.3 bcm in January 2022, hitting a new monthly low record as shown in Figure (2) below.

According to the EOA’s calculations, Gazprom transported 1 bcm of gas through Ukraine (Sudja gas station), of which 0.2 bcm was consumed locally in Ukraine while the remaining 0.8 bcm was sent to the EU. Gazprom also exported another 0.8 bcm of gas to the EU via the TurkStream pipeline connection with Bulgaria. In total, Gazprom exported a low record of 1.6 bcm of gas in January 2023 to the EU member states which is equivalent to an annual figure of less than 20 bcm. Back in 2022, the EU imported around 60 bcm of gas from Russia via pipelines.

Figure (2)

Under current conditions, Gazprom can export gas only through two remaining routes: Ukraine via the Sudja gas station, and the TurkStream pipeline. Gazprom’s gas supplies through the Nord Stream 1 and Yamal-Europe gas pipelines have been stopped since last year. Together, they had a total capacity of 88 bcm annually which is no longer available on the back of a dispute between Russia and the EU, and due to attacks on the Nord Stream 1 in late September which put the undersea pipeline out of service as illustrated in Table (1) below.

Table (1)

Status of Russian Gas Supply Routes to EU

Source: EOA 2023

Norway

Norway is currently the EU’s main gas supplier accounting for more than one-third of its total gas imports. The EOA’s calculations show that Norway shipped 8.96 bcm of gas to Germany, Belgium, France, and Denmark last month.

For most of January, Norwegian gas exports to Germany remained at historic highs of more than 140 million cubic meters per day as Germany looks to replace lost Russian gas. Gas exports to France, meanwhile, averaged close to 38 million cubic meters per day.

The production of natural gas in Norway is projected to continue at the same level for the next 4-to-5 years, according to the Norwegian Petroleum Directorate (NPD) where it is currently producing at its maximum at 122 bcm annually.

Azeri Gas Exports on the Rise, Unlike North Africa’s

Azerbaijan supplies Europe with natural gas via the Trans Adriatic Pipeline (TAP). The EOA’s calculations show that Azerbaijan increased gas exports to the EU in January to some 1 bcm, a 20% record increase year-on-year (YoY).

It is obvious that Baku is on track to hit last year’s annual record figure of 11.6 bcm. In July 2022, the EU signed a deal with Azerbaijan by which the latter has committed to double its gas exports to the bloc to 20 bcm of gas annually by 2027.

From North Africa, the EU received 2.3 bcm of gas in January, mostly from Algeria which exported 2.06 bcm to Italy and Spain. For its part, Libya kept its monthly gas exports to Italy through the GreenStream pipeline to its lowest level down to 200 million cubic meters. Last year, Libya exported some 2.4 bcm of gas, the lowest figure in a decade.

LNG Taking the Lion’s Share

LNG has proved to be a viable option to help the EU increase its security of gas supply. Without LNG, it would have been impossible for Europe to reduce its reliance on Russian gas. In January, the EU’s LNG imports totaled 7.4 million tons (equivalent to 10.2 bcm), a 1.5% uptick YoY. The European appetite for LNG was lower in January than in previous months, thanks to the above-normal gas storage level that stood at 83% at the beginning of the year.

Looking at the full picture, LNG accounted for the lion’s share of the EU’s total gas imports in January or 42%, followed by Norway at 37%, while Russia (excluding its LNG exports) has retained only a little share of 7% of total EU gas imports as shown in Figure (3).

Figure (3)

LNG and additional gas supplies from key producers like Norway have helped the EU reduce its reliance on Russian gas. This would not have happened without other EU measures aimed at reducing gas demand in member states. The second half of this year, however, could be the real test when EU member states start filling their gas stockpiles to prepare for the next heating season, which could be challenging with the current low flows of Russian gas.